Help I own a STONK!

Cloudflare: A Great Business with Sky-High Expectations

Cloudflare: The superb business that's gone from hidden software gem to full-blown STONK 🚀

Disruption playbook: How to build a $26bn company by reimagining internet infrastructure

The psychological rollercoaster of holding something on 23.5x EV/Sales

Mr Market is offering me a high price but can I really find a better business?

Investor's dilemma: Hold a phenomenal business or cash out before the hype train derails?

Cloudflare is a long-term holding and currently the biggest position in the Northwest Frontier portfolio. I continue to believe that Cloudflare is one of the best positioned listed technology companies, with a credible opportunity to be a +$1 trillion company in the future. However, despite substantial increases in intrinsic value, most of my returns from the position have come through investors' re-rating of the shares. A quick check of X and Reddit demonstrates just how hyped Cloudflare has become.

Now trading on 23.5x EV/Sales, I am faced with a real dilemma. I want to continue to own a business with a high-quality platform business that is powered by some unique network effects, a business with a model designed from the ground up to disrupt its competition in some of the largest markets in the world. However, how can I hold a stock where heightened expectations have pushed valuation to close to the farthest it can go. In essence, what do you do when the fundamentally great business you own turns into a STONK.

Why is Cloudflare such a good business?

Let me introduce Cloudflare a bit more. The company is a $49bn market cap provider of computer networking software. Cloudflare occupies a critical position in today's internet infrastructure stack with its services currently powering around 20% of all websites worldwide. The network it has built is highly differentiated, giving the company a series of unique competitive advantages. In addition, it has some of the best structural growth opportunities in software, with an addressable market opportunity of $222bn. The company can then combine this with superb economics that point towards a highly free cash-flow generative future.

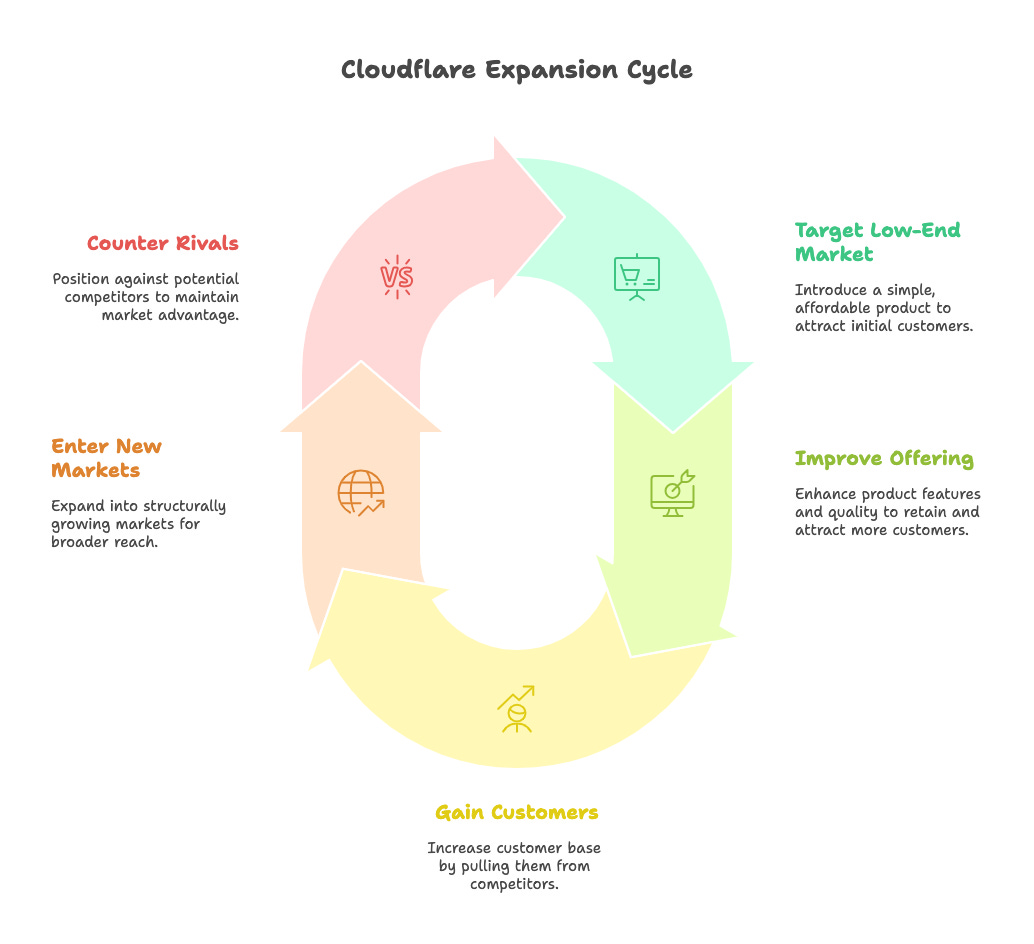

Designed to Disrupt

The company's fundamental strength lies not in a single competitive advantage, but in a meticulously constructed ecosystem of technological innovations. By pioneering software-defined networking (SDN), Cloudflare engineered a distributed edge network that fundamentally reimagines how computational resources can be deployed globally. This architectural approach isn't just technically impressive—it's strategically brilliant. The company has systematically built a modular platform that creates significant barriers to entry for potential competitors, while simultaneously maintaining remarkable cost efficiency.

Cloudflare's growth strategy epitomizes Clayton Christensen's disruption theory: enter markets with price-competitive, elegantly simple products, and then rapidly evolve the offering. From content delivery networks to DDoS protection, serverless computing, and zero-trust security, the company has methodically expanded its footprint. Each horizontal expansion isn't just a new product line—it's a calculated move to capture emerging market opportunities while strategically positioning itself against potential rivals.

What makes Cloudflare truly exceptional is its structural design for disruption. Unlike traditional infrastructure providers, the company has created a platform that is simultaneously scalable, adaptable, and cost-effective. Its network effects aren't just technological—they're systemic. By continuously expanding and improving its offerings while maintaining a modular, software-driven approach, Cloudflare has positioned itself not just as a service provider, but as a potential architect of future internet infrastructure. The company doesn't just compete in markets; it reimagines how those markets could fundamentally operate.

Growth opportunities

Cloudflare offers multiple products under one single platform, each of these products are often multibillion software verticals and where Cloudflare demonstrates several significant competitive advantages. I will focus on 3 notable examples:

Content Delivery Network (CDN): CDNs crucial for website speed and data transfer, is experiencing massive growth driven by richer internet content and diverse devices. Valued at $32 billion today and doubling in the last five years, the market is projected to continue expanding at 17% annually until 2030. Cloudflare has capitalized on this expansion by offering a CDN product significantly cheaper (7x less) than competitors like Fastly. While Fastly focused on high-end enterprise clients with premium pricing, Cloudflare targeted a broader market, including smaller customers. This highlights a classic innovator's dilemma, where incumbents struggle to disrupt themselves by offering lower-margin products, leaving Cloudflare well-positioned to dominate the burgeoning CDN market.

· SASE (Secure Access Service Edge): This is the market for cloud-based solutions to securing computer networks. Estimates by Gartner suggest the market will grow at a 29% CAGR to 2027, reaching over $25 billion in annual spend. SASE emerged as a response to the limitations of traditional network architectures to threats that have emerged from more corporate data being hosted on the cloud and accessed through the internet. Cloudflare has built a unique position in the SASE by taking advantage of its network infrastructure to build an entirely organic, integrated SASE product set within one platform. By contrast SASE incumbents, like Palo Alto, have been built via acquisition and rely on running their services on external network providers. This gives Cloudflare the ability to offer services

Cloud Developer Platform: Cloudflare ability to run a distributed computing network also allows to offer compute services, like Hyperscale’s like AWS in innovate ways. Because of the efficiency of Cloudflare’s cloud infrastructure, they can offer more flexibility to customers in how they consume compute. Cloudflare isn't competing directly with the full-service offering from hyperscale’s but creating a foundation for a modular cloud ecosystem where customers can freely move data between best-of-breed services for cloud development. Hyperscale’s struggle to respond without undermining their profitable integrated model. For example’s Cloudflare’s R2 storage product eliminates egress fees (costs to move data out of a cloud environment) which AWS charges at up to 7959% margins. This kind of differentiation gives Cloudflare a credible chance at disrupting the $54bn cloud application development market.

AI: Cloudflare is also finding structural opportunities in AI. Their edge network positions Cloudflare as a source of scalable compute capacity, a critical element of running AI services. Cloudflare has also leveraged this scalability to offer pay-as-you-go pricing, unlike competitors who make consumers purchase computing capacity upfront, dramatically cutting costs. The reliability of Cloudflare's network is perfectly suited to running AI agents, offering customers a robust AI platform without the need to manage complex technical infrastructure themselves. The company’s security capabilities have also enabled Cloudflare to offer additional services. It is widely believed to be a partner of Apple’s on its private cloud relay (a potential $100m opportunity alone) and it also has the leading AI firewall solution. AI is simply driving more demand across Cloudflare’s platform.

What underlines each of these opportunities is built upon the same infrastructure. everything Cloudflare provides is from a unified platform, technology stack and code base. By solving multiple problems through the same infrastructure, they create increasing returns on capital while having a lower marginal cost to ship product. There are some major benefits to this structure, increasing relevancy with customers, growing network effect and superb economics that point towards a highly recurring, highly free cash flow generative business model.

Subscription Model: The Foundation of Durable Growth

Cloudflare may have multiple areas for growth, but it has a simple and predictable economic model.

Cloudflare's business is built on a subscription model that creates an exceptionally strong foundation for durable growth. This highly recurring revenue stream provides predictability, a great feature in a business, but more importantly, it reveals a fundamental truth about the company's relationship with its customers. The key metrics that matter for subscription businesses—churn and net revenue retention (NRR)—tell a compelling story here. Less than 10% of customers leave each year and a NRR of 111% Cloudflare's customers stick around and spend more over time, indicating not just satisfaction but genuine dependency on the company's services.

What makes this model particularly powerful is how it leverages Cloudflare's inherently efficient architecture. A distributed network with standardized hardware running unified software, creates economies of scale that drive inherently high margins. However, if you're just looking at their P&L statements, you might miss the true margin potential of the business. Like most SaaS companies, Cloudflare bears costs upfront while revenue trickles in over time, making the P&L a backward-looking indicator rather than a window into the future.

The beauty of Cloudflare's model is that as revenue compounds, those centralized costs don't grow proportionally. Each new dollar of revenue requires less marginal cost to service, creating a margin expansion engine that should become increasingly obvious over time. The subscription model isn't just about recurring revenue—it's about building an economic machine where revenue growth outpaces cost growth by design.

Source: Company presentation

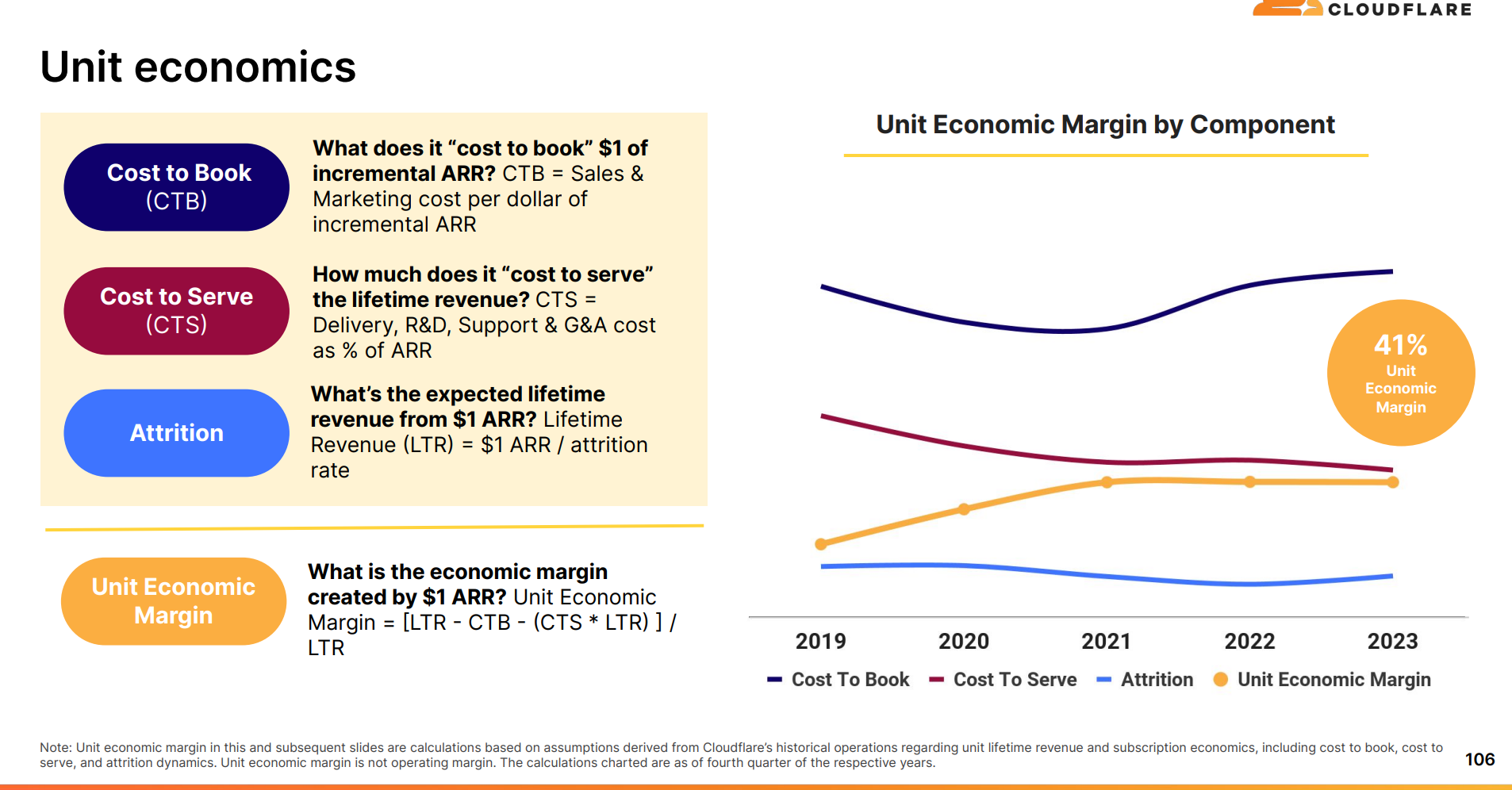

Unit Economics: The Hidden Profit Machine

Drilling down into Cloudflare's unit economics reveals why investors should be excited about its future. When you focus on the fundamentals—cost to acquire customers, cost to serve those customers, and customer retention—the picture becomes clearer. Cloudflare already generates 41 cents in economic profit for every dollar of subscription revenue. This is the key metric that matters, not the GAAP accounting that weights towards cost borne today versus revenue recognised over time.

What's particularly interesting about Cloudflare's model is how consumption drives better retention and increased spending. As customers integrate more Cloudflare services into their technology stack, switching costs rise and the value proposition becomes more compelling. This creates a symbiotic relationship where increased consumption leads to higher retention, which in turn creates more capacity for Cloudflare to develop new products, thereby increasing consumption further.

Source: Company presentation

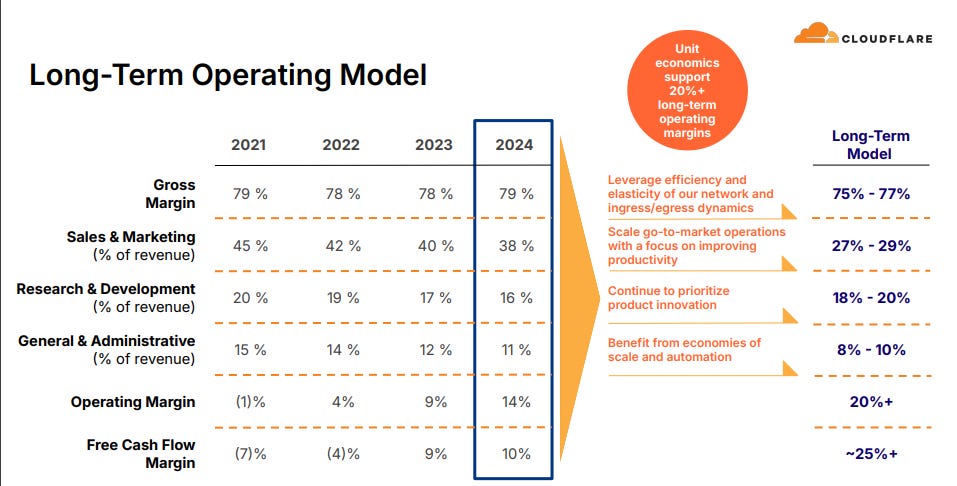

This virtuous flywheel is the heart of Cloudflare's economic model. As customers adopt more services, they spend more over longer periods, generating higher margins that Cloudflare can reinvest in product development. Cloudflare's largely fixed cost base means this flywheel will eventually generate significant free cash flow. The company is targeting a operating with >20% margin, all built upon an increasingly loyal and locked-in customer base. The compounding effects of this model are still in early innings but point to extraordinary long-term economics.

Strong Execution: Turning Theory into Practice

Cloudflare isn't just sitting back and waiting for this flywheel to spin—they're actively accelerating it through clever go-to-market strategies. Their innovative approach to customer contracts exemplifies this proactive stance. The company has been pushing what they call "pool of funds" deals, where customers purchase spending commitments that can be allocated across any of Cloudflare's products.

This strategy is particularly shrewd because it leverages the architectural flexibility that Cloudflare has built. Unlike competitors who might have disparate products running on different infrastructure, Cloudflare's unified architecture allows customers to seamlessly adopt new services. By securing larger upfront revenue commitments while simultaneously encouraging customers to experiment with different products, Cloudflare increases both immediate cash flow and long-term engagement.

These spending commitments kick-start the economic flywheel by driving higher attach rates across Cloudflare's product portfolio. Customers can as easily consume CDN services as they can explore Workers, Zero Trust, or other offerings, becoming more deeply integrated with Cloudflare's ecosystem with each new service they adopt.

As these forces compound over time, the company is positioning itself to generate the kind of high-margin cash flows that define the most successful technology businesses. The subscription model provides the foundation, the unit economics drive the engine, and smart execution accelerates the journey toward what looks increasingly like a very profitable future.

Cloudflare's Execution: Building Momentum on Strong Fundamentals

Because Cloudflare has so much potential in both growth and margin progression, much of my investment analysis focuses on finding concrete evidence that they're executing against this opportunity. In technology businesses with subscription models, customer metrics serve as leading indicators of future performance, particularly the acquisition and expansion of larger customers. These enterprise customers not only validate Cloudflare's model in the most demanding environments but also offer significantly more revenue opportunities through their complex needs and larger budgets.

Q4 2024 provided compelling evidence that Cloudflare's execution is accelerating across several critical dimensions. The company reached 237,700 paying customers, adding a record 48,000 new customers in 2024—representing 25% year-over-year growth. More impressively, Cloudflare added 3,500 large customers, with a record addition of 740 large customers throughout 2024 (27% year-over-year growth) and 232 large customers in Q4 alone. The revenue contribution from these large customers increased to 69% of total revenue, up from 66% in the fourth quarter of the previous year.

Beyond raw customer growth, Cloudflare is showing signs of increased operational efficiency. The company delivered a 10-percentage point increase in ramped Account Executive quota attainment, achieving over 80% compared with 2023. Most of these gains came in the 125% or higher attainment cohorts, suggesting that the sales organization is becoming more effective at closing larger deals and expanding existing accounts.

The company's current Remaining Performance Obligation (cRPO) growth outpaced revenue growth, showing the strongest sequential growth in three years. This forward-looking measure of contracted business suggests accelerating momentum that hasn't yet appeared in reported revenue figures.

What makes these metrics particularly compelling is what they signal: customers are increasingly recognizing the value of Cloudflare's platform approach. As enterprises acknowledge this value proposition, they commit to larger initial contracts and expand their usage over time. Combined with improved sales productivity, there's a sense of genuine momentum building within the company.

The Investment Case Strengthening

The broader point here is that there's mounting evidence suggesting Cloudflare is successfully executing against its massive opportunity. Customer numbers are accelerating, those customers are getting larger, and Cloudflare is achieving this growth with increasing efficiency. If we focus purely on the fundamentals, this looks like a successful investment thesis playing out, with considerable runway remaining given the size of Cloudflare's addressable market.

The network effects embedded in Cloudflare's model mean that as they add more customers and expand their network, the value proposition for future customers improves. Each new customer deployment teaches their systems and improves their security capabilities, while expanding the network's reach reduces latency for all users. This creates a virtuous cycle that should continue to compound.

What's clear from these metrics is that the company isn't just talking about potential—they're delivering measurable progress quarter after quarter. For long-term investors, that execution against fundamentals matters far more than short-term valuation concerns, especially for a company like Cloudflare that's still early in capturing its opportunity.

The trickier question is what to do when improving fundamentals raise expectations about the future. Cloudflare already trades at a premium multiple relative to peers, reflecting the market's recognition of its superior model and execution. The challenge is what to do when whether the improving metrics just fuel ever higher investor expectations.

The Valuation Conundrum: When Success Becomes Complex

Few narratives capture the nuanced tension between fundamental business strength and market expectations quite like Cloudflare's current economic position. Trading at an eye-watering 23.6x EV/Sales multiple—a staggering 119% increase from my initial investment in May 2023— however even extraordinary businesses ultimately cannot sustain ever increasing investor expectations and there are risks to the position should the company disappoint.

Cloudflare EV/Sales multiple, 2020-2025

Source: Koyfin

The core of Cloudflare's compelling story (and my investment) lies in its unique positioning within structural growth markets. Unlike traditional technology companies constrained by linear expansion, my thesis is Cloudflare has cultivated a business model with on non-linear growth potential. This isn't mere speculation, but a strategic hypothesis grounded in the company's ability to leverage network effects and infrastructure innovation. By targeting markets with an average compound annual growth rate (CAGR) approaching 20% through the end of the decade, Cloudflare isn't just participating in technological evolution—it's attempting to reshape fundamental internet infrastructure.

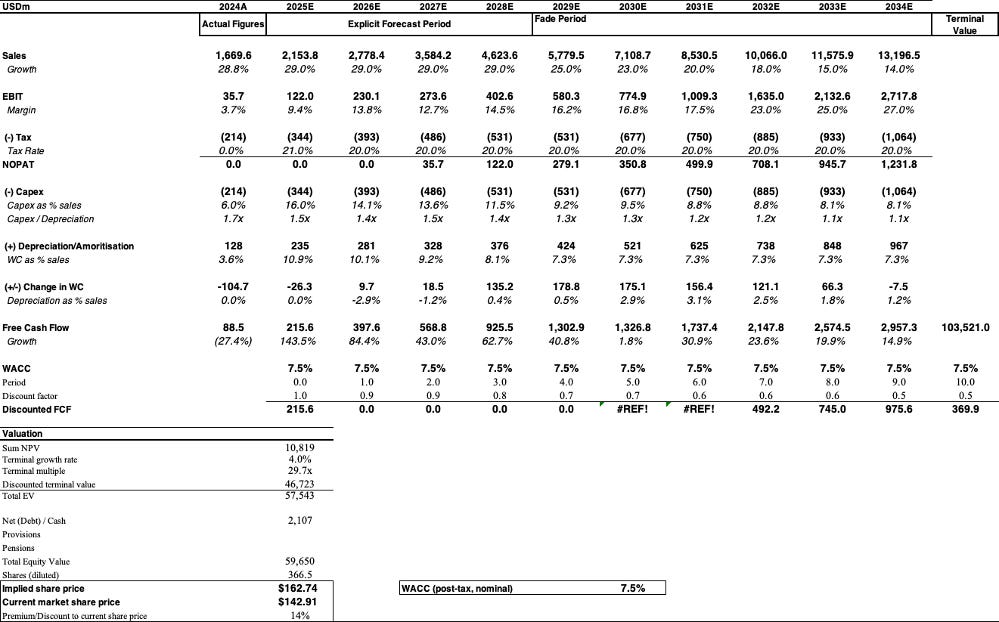

A quick demonstration of the fundamentals shows even heighted valuation for Cloudflare has some underpinnings. A basic discounted cash flow (DCF) analysis—admittedly I am using an over simplified example here but illuminating—suggests that under specific assumptions, Cloudflare could still offer upside. Projecting a scenario where the company maintains over 25% CAGR for the next five years, subsequently moderating to low teens growth, and achieving 30% operating margins by 2034, the analysis produces approximately 15% potential stock appreciation. This is an aggressive absolute scenario but is still predicated on a modest market share assumption: even at this optimistic forecast, Cloudflare would only capture roughly 5% of its addressable total addressable market (TAM) by the decade's end.

Cloudflare DCF

Source: Company reports, NWF estimates

Originally the edge on Cloudflare lay in recognizing that structurally Cloudflare had the ability to product growth in a way the market had failed to recognise. Now however, the current valuation demands more precise forecasts of fundamental outcomes. The analytical challenge of valuing Cloudflare has shifted from identifying overlooked value to navigating an increasingly narrow and inherently unreliable corridor of growth expectations.

The Psychological Dilemma of Never Sell

Sitting with my Cloudflare position feels like being trapped in an intellectual maze of my own making. It's easy to criticize overvalued stocks from the sidelines, but when you're actually holding a position that has performed brilliantly, the psychological barriers of endowment bias become viscerally real. The company's story remains extraordinary, and my portfolio's performance is a testament to its strength—which makes the current decision exponentially more challenging.

The fundamental tension lies in the opportunity cost. Cloudflare's valuation has pushed into rarefied territory, yet the underlying business fundamentals still—just barely—justify continued ownership. Cloudflare will continue to show high IRRs in fundamental terms, should the valuation fall it would like justify re-entering the name. Selling now feels like an act of market timing, potentially exchanging a proven performer for uncertain alternatives. Especially difficult when I am unlikely to find a business as capable as Cloudflare. Mr Market is offering a high price for this wonderful asset, but there isn’t the ready opportunity to to find more wonderful assets.

My conclusion is both a philosophy and a commitment: I am a fundamental investor who views ownership as stewardship. While the internal rate of return might be diminishing, I'm willing to bear short-term underperformance if the long-term fundamentals remain intact. However, I cannot and will not ignore the increasing precision required in growth forecasting and the risks associated forever.

This isn't about blind loyalty, but strategic patience. My portfolio is a business, always seeking the highest returns. I remain open to cycling capital into new ideas with superior potential, but for now, Cloudflare remains a core holding. But I readily admit I wracked with doubt. To any fellow investors wrestling with similar dilemmas: I'm all ears for perspectives that might illuminate this complex decision!