The Lululemon long game

Looking beyond Q1 guidance to find value in a premium brand

Despite disappointing Q1 guidance, Lululemon's fundamentals remain strong with robust margins and healthy cash flow

Product innovation and "newness" are resonating with customers, maintaining conversion rates and increasing average order value, providing strong underlying foundation for growth

International growth of over 20%, particularly in China, continues to drive growth while North America faces cyclical challenges

Management's focus on strategic marketing and inventory management has maintained sector leading margins of >20%.

Trading at its lowest valuation in 10 years while still outperforming long-term targets set in FY21

One of the most fascinating aspects of the apparel and athletic-wear space is its continuous tug-of-war between brand strength, macroeconomic conditions, and the evergreen question of growth sustainability. Lululemon, an industry leader in premium activewear, recently reported Q4 earnings that highlight these tensions in a way that speaks volumes about both the brand's near-term challenges and its long-term potential. While the company did offer some disappointing guidance for Q1, the context is crucial: there are real macro headwinds, but the fundamentals remain impressively strong. The company's competitive response on product has been somewhat overlooked, margins remain strong and cashflow is robust. Management highlighted that the company is focusing "on what we can control" and with a lot of evidence of execution on this there is still a lot to like in the long-term picture.

Contextualizing Q4 vs. Q1

Lululemon reported better than expected Q4 2024 numbers but issued disappointing guidance for Q1 and full year guidance for FY 2025. Q4 revenue was $3.6bn, an increase of 13% year-over-year, driven by flat comparable sales in the Americas and 20% growth internationally. EPS was $6.14, driven by strong gross margin performance. The company guided toward revenue of between $2.335-2.355B for Q1 and between $11.15-$11.3B for FY 25, which was respectively below -2% and -1% below current expectations. CFO Meghan Frank also commented that the company expects LSD-MSD revenue growth in the Americas (with the US at the lower end of the range and Canada at the higher end**)**. EPS is expected to be between $2.53- $2.58 in Q1 and $14.95-$15.15 over FY 25, below expectations by -7% and -2% respectively. The weak guidance has led to renewed concerns about its growth profile, and in particular its North American performance.

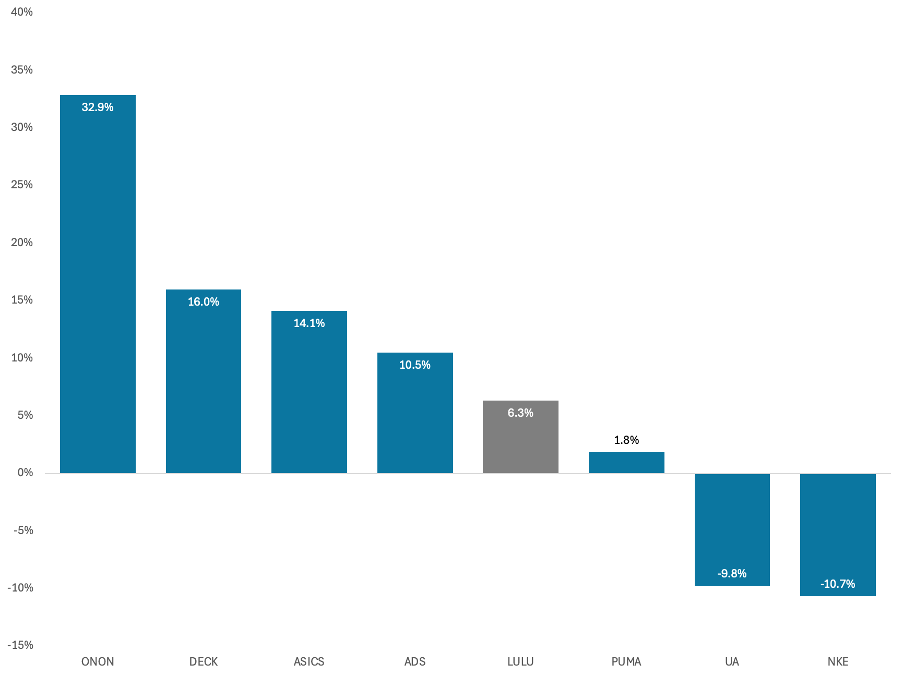

The management team was explicit in noting that the biggest driver of weaker Q1 guidance is softer traffic in North America. They attribute this slowdown partly to macro uncertainties, such as inflationary pressures and general consumer hesitancy, impacting consumer confidence, as well as to challenging comparables in Q1 from the prior year. Yet, Lululemon's performance still surpasses that of many in the retail and athletic-wear sector, indicating that the brand's strength is a mitigating factor in the face of a more uncertain environment.

Sports Consumer Discretionary Peer Group, NTM sales growth forecast.

Conversion, AOV, and the "Newness" Factor

While traffic may be declining, one of the reassuring signals from the report is that conversion rates remain consistent. In other words, those who do walk into Lululemon's stores or browse online are just as likely to purchase as before, which points to a stable and engaged customer base. Even more promising is the increase in average order value (AOV). Higher AOVs can be a function of multiple factors: more premium-priced items, effective upselling strategies, or stronger brand loyalty. Lululemon's management made clear that the initial steps to revitalize and inject newness into the company's line are resonating with customers, and marketing initiatives are delivering solid results. CEO Calvin MacDonald highlighted:

"Looking at quarter one, we have increased our level of newness on par with the past. We believe this increase along with a robust pipeline of innovation will enable us to meet the expectations of our guests and I'm excited about what the product teams are bringing to market this spring throughout the year. We started the year strong with the launch of several new innovations.

Initial response has been very strong, and we've been selling out across several sizes and colours. The teams are chasing into it now and we have several additions planned for later this year. Based on this response and performance, we believe Daydrift will become a new core franchise."

It's important to remember that concerns throughout 2024 were on the competitive pressures that Lululemon's faced from Alo or Vuori. These comments indicate Lululemon has effectively defended its position against would-be challengers, consumers are still clearly engaged with the brand and product initiatives. There is an argument that a successful competitive response by Lululemon is being overlooked as markets' attention has shifted from competition concerns to broader concerns about macroeconomic conditions and consumer spending patterns. For all the commentary around Lululemon, the story may in fact be quite simple, with the company navigating short-term headwinds with a robust underlying business. Traffic trends in North America may be weaker, but the brand's ability to maintain conversion and even boost AOV are encouraging structural signs. Concerns around the company are looking increasingly cyclical. Not only is this a stronger position than when competition was the main debate, but with Lululemon's FY guidance effectively assuming traffic trends from Q1 persist for the entire year, it may give some room for outperformance.

International Remains Robust, with China Leading the Way

Given concerns over the US, what's perhaps underappreciated—is the continuing strength of Lululemon's international performance, particularly in China. Management noted no signs of a slowdown in international traffic, especially in China, which remains a critical growth driver. This was in a quarter where many global brands reported shaky results from their overseas markets. A quick comparison of Lululemon's China numbers against those of Nike's demonstrates there is still stellar relative performance being produced by Lululemon's brand.

China yoy Sales growth LULU vs NKE, Q4 23 - Q4 24

Of course, international is not a monolith. While China boasted robust growth, the rest of the world saw a noticeable slowdown during the quarter. Comparable sales grew 14% during Q4, down from 23% in the prior quarter. The company did not offer a concrete explanation on the call for why certain regions weakened, but management guided to a rebound with 20% growth in Q1.

Long-Term Potential and Margin Benefits

What I believe is that from a strategic standpoint, Lululemon's international expansion continues to be overlooked. Though the segment still remains 22% of sales, it is gaining 2pp of sales contribution annually and offers a favourable business mix that can elevate gross margins and operating leverage. The relatively untapped potential in regions like the rest of Asia Pacific and Europe opens a wide runway for future growth. McDonald again illustrated the low penetration the company has in international markets:

“Our unaided brand awareness in France, Germany and Japan is in single digits. In China Mainland, it's in mid to high teens. In the UK and Australia, it's in the 20s and in the U.S, unaided brand awareness is in the 30s.

This international performance also speaks to the strength of Lululemon's core brand. If there were fundamental issues—stagnation in product appeal, diminishing brand relevance, or subpar execution—we would likely see cracks forming in new markets, where consumers are less entrenched. Instead, the opposite is true: the company's international figures show a brand that is resonating strongly, this remains a powerful growth driver for Lululemon over the long-term even though focus may be on the temperamental short-term dynamics in the US.

Margins: A Testament to Inherent Strength

One of the most telling indicators of Lululemon's health is its gross margin performance. While the company started the fiscal year guiding for flat gross margins, it ended up delivering a 65-basis-point expansion. In a retail environment rife with discounting and promotional pressures, expanding gross margins is a remarkable feat. Management attributed this outperformance to a favourable product mix shift towards higher-value items and a disciplined approach to markdowns. While Lululemon is guiding down gross margins by around 60 basis points for 2024, more than half of this headwind comes from one-off factors like tariffs and foreign exchange (FX). These are externalities, rather than signs of internal weakness. The underlying dynamics—such as increasing order values—still point to a robust long-term margin profile. These factors do not appear to compromise the structural margin advantages Lululemon enjoys. The company's ability to keep AOV on an upward trajectory is another margin driver. Consumers are willing to pay for Lululemon's product innovations, whether that's a new type of performance legging or expansions into men's apparel and accessories. Over time, this willingness should continue to support healthy gross margins, even if short-term volatility persists.

EBIT Margins and the Role of Marketing

Much like gross margins, Lululemon's EBIT margins told a tale of two timelines: Q4 was better than expected, but the guidance for upcoming quarters is less optimistic. A key factor here is the continued investment in marketing, particularly in what the company calls its "activation strategy." Essentially, Lululemon is choosing marketing spend at around 5% of sales to ensure brand visibility and product awareness, it maintained this even in a period of weaker new product launches last year. Management emphasized that these marketing campaigns were still successful, helping drive traffic and sales during the critical holiday season. It gives the impression that sustained high marketing spend may have covered the company from even weaker sales, given the product weakness. Looking ahead to 2025, management is planning to combine this heightened marketing investment with renewed product newness. CEO Calvin McDonald commented:

“We're always testing and learning and looking for ways to continue to invest within the parameters of our guidance to add to marketing. And I think I'm very pleased with the current response from our guests, excited about the campaigns coming……..

…….as I mentioned, the cadence and rhythm to start this year has been definitely on the offense. And I'm pleased with the results and those results around the globe. And we're going to continue to be on offense and support the product and the pipeline of newness that's coming and with our guests.”

This could be a potent combination. Product innovation often provides a jolt to sales, and when paired with robust marketing, it can lead to an outsized return on investment (ROI). The buzz around a novel product line while saturating key channels with effective campaigns has been missing from Lululemon marketing efforts for well over a year, and the synergy could boost both top-line growth and profitability. Of course, marketing investments carry risks. The company's guidance acknowledges that should the macro environment deteriorate further, contingency plans are in place to protect margins. Yet, in the broader context, Lululemon remains one of the most efficient operators in its sector, converting a large proportion of gross profit to EBIT. The argument that these margins are unsustainable has circulated for years, but so far, the company has consistently demonstrated that its cost structure, pricing power, and brand appeal are sufficient to maintain a high level of profitability.

Sports Consumer Discretionary peer group LTM EBIT/Gross Profit conversion

If demand truly collapses, management can pivot, scaling back on certain campaigns or delaying specific initiatives. But for now, they are making a calculated bet that sustaining and even amplifying brand presence is the better course of action. This signals confidence in the product roadmap and the overall brand proposition, reinforcing the idea that near-term headwinds are cyclical rather than structural.

Cash Flow and Uses of Capital

Finally, we come to cash flow, an often overlooked but critical piece of the puzzle. One of the most telling aspects of Lululemon's Q4 results was the better-than-expected inventory performance. Inventories ended up only 9% higher than the prior year, as opposed to the low double-digit (LDD) growth the company had guided. For Q1, Lululemon is targeting high-teen inventory growth, specifically to chase product "newness," which underscores the company's confidence in upcoming collections. The CFO also expressed strong confidence in both the level and the mix of inventory, which is not what you'd expect from a brand struggling with relevance.

Lululemon's solid margin profile and tight inventory management have fuelled remarkable free cash flow (FCF). The company has generated $3.2 billion in cumulative FCF over the last two years, and management anticipates another $4.8 billion over the next three years, even if growth remains in the mid-single-digit range. This is a staggering figure, especially for a retail company that was once dismissed as a niche yoga brand.

The company's most significant use of capital currently is its share repurchase program. Last quarter, Lululemon bought back $332 million worth of shares, reducing its share count by 3.7% year-over-year. Over time, this kind of consistent buyback activity can meaningfully boost earnings per share (EPS). In fact, management believes that using the projected $4.8 billion in FCF for buybacks over the next three years could add as much as 13% to EPS. This is no small feat, especially if sales growth hovers in the mid-to-high single digits. When you step back, Lululemon's strong cash flow position underscores a theme that runs through this entire analysis: optionality. The company can afford to invest in marketing, open new stores, optimize existing ones, and expand internationally, all while returning capital to shareholders. This level of flexibility is a hallmark of a well-run business, particularly in a sector as volatile as retail. When macro conditions improve, Lululemon will be poised to accelerate its growth. In the interim, the extent to which its cashflow can build. A path back to double-digit EPS growth even if top-line growth temporarily slows is also a potential tool.

Conclusion: Balancing Short-Term Turbulence with Long-Term Optimism

Overall, the real debate here seems to center on whether Lululemon's current slowdown in growth is cyclical or structural. My view is that there is a clear collection of factors pointing to a cyclical challenge: macro conditions, tariffs, and FX headwinds are weighing on consumer sentiment and company guidance. However, none of these factors undercut the fundamental strengths of the brand. Competition from Alo or Vuori has not derailed Lululemon, and the company's success in China demonstrates its global relevance. Meanwhile, gross margins and EBIT margins continue to signal a healthy, profitable business, even in a tough environment. Equally important is the company's strategic positioning for the future. Between continued marketing investments and renewed product newness, Lululemon appears poised to capitalize on any improvement in consumer sentiment. Internationally, there is vast white space in Asia Pacific and Europe. All the while, the company's free cash flow generation and share buybacks create a floor for EPS growth.

Management's conservative guidance reflects a prudent reading of current conditions, but it does not alter the underlying thesis: Lululemon's brand strength, operational discipline, and strategic flexibility position it for success once the macro clouds part. For investors and observers, the key is to focus on the bigger picture. Yes, short-term volatility will continue, and yes, the market may penalize any sign of weakness in retail. But if you believe in the longevity of Lululemon's brand, its long-term growth prospects remain largely unchanged. For all the travails surrounding Lululemon it in fact remains ahead of its long-term targets set in FY21, despite this the stock trades at its lowest valuation in 10 years.

Lululemon Sales versus Power of Three 2x Long-term Targets, FY21-FY26

Lululemon P/E ratio, 2015-2025

Lululemon has repeatedly demonstrated the ability to adapt, expand, and capture market share, even when conditions are less than ideal. The short-term noise might be loud, but the long-term signal remains one of strength and potential.