YouGov's Inflection: Shakespeare's Return & the Path to Recovery

With sales stabilising in H1 and a clear refocus underway, the company looks compelling on a 14% FCF yield

The return of Stephan Shakespeare, and the renewed strategic focus he is implementing, marks a significant inflection point for YouGov

YouGov is refocusing on its platform-based approach, significantly refreshing products and revamping its go-to-market approach.

On just 9x P/E and 14% FCF yield, the company is priced like a structurally declining asset. However, YouGov’s cost restructuring plan alone will deliver >40% EPS growth over the next 18 months.

Despite execution concerns, YouGov remains a +20% EBIT margin company with a leading offering in the $54bn Market Research industry. Between new AI products, dedicated sales efforts for Data products and the synergies with CPS, there are multiple opportunities to drive long-term growth.

H1 could ultimately mark an inflection point for YouGov, marking the return of its founder CEO armed with a mandate for change. The narrative isn't straightforward; it's a complex interplay of stabilizing the core, revitalizing product and reinforcing a platform-based strategy, all under the shadow of a cautious market.

Stephan Shakespeare's return to the CEO role isn't merely a C-suite shuffle; it feels more like we have seen recently. The reinstatement of a charismatic leader (and original architect) tasked with a second term focused on restoring better times. While I have been critical about leadership changes at the company, I have learned from H1 results that this isn't just an interim appointment about finding another successor. The signal seems clear that Shakespeare is back with a definitive, arguably founder's, mandate.

The objective extends beyond steadying the ship; it's about steering YouGov back towards its foundational strategy, perceived by Shakespeare to have drifted, and executing with renewed discipline. The core task appears threefold: re-aligning the strategic course, fixing the product roadmap, and ensuring execution follows intent. This context is crucial – as YouGov is now setting a deliberate course correction toward refocusing on its core platform with a blueprint to improve its importance. It is slowly becoming clear that YouGov's core offering remains sound but was lost in the translation of a management transition and/or execution missteps. The challenge, of course, is if the organizational structure can execute effectively under this renewed direction.

Sales: Finding the Floor, Building the Base

The narrative around YouGov's sales is one of cautious stabilization, a necessary precursor to any talk of resurgence. The trends have undeniably been muted, a reflection, management suggests, of previously discussed headwinds hitting execution. However, the critical message from the earnings report is that the situation appears to be bottoming out; the bleeding has stopped, or at least slowed to a trickle, and perhaps more importantly, the foundation remains stable.

This stability primarily rests on the performance of existing renewals in Data Products. With the majority of total existing customer contracts for FY25 already secured during the period, YouGov has established a predictable revenue base for the immediate future. The reported renewal rates, holding firm at historical levels above 80%, are testament to the stickiness of the core subscription offering. This isn't trivial; in a subscription business, retention is the bedrock upon which all future growth is built. It signals that despite recent challenges, the core value proposition still resonates with a large portion of the customer base.

From this base, the key variable for near-term performance becomes pricing. Any price increases successfully implemented during these recent renewals will flow directly into revenue growth, particularly in the second half of the fiscal year. This is where the mechanics of subscription revenue become particularly relevant. New sales, while important for long-term health, often have a diminishing impact within a given fiscal year due to phasing – a contract signed mid-year only contributes partial revenue. However, price increases on the existing, already renewed customer base have an immediate and full impact for the duration they cover, in this case, H2. As consensus currently estimates virtually no growth for the remainder of the year, this dynamic underpins the potential for upside surprises relative to guidance, even if new business acquisition remains sluggish.

YouGov Segmental H1/H2 Revenue breakdown

The macro environment, however, looms as a significant concern for investors. The potential for softer economic conditions, coupled with ongoing uncertainty around factors like tariffs, could theoretically dampen customer confidence and spending on data and insights. However, management projected relative confidence on this front, highlighting that customer dynamics haven't materially changed since their February updates. In addition, I would also make the parallels to the COVID period, where YouGov demonstrated resilience even during peak uncertainty, implying the core business isn't immediately susceptible to macro shocks impacting customer retention.

Furthermore, the segment arguably most sensitive to economic downturns – Data Services, characterized by more discretionary, project-based work – has already experienced significant declines. This suggests that much of the potential macro-driven pain in that specific area may already be baked into the current run-rate, limiting its potential to be a further drag on overall performance moving forward.

However, stabilizing the base is different from accelerating growth. Management acknowledges that a significant uptick requires more than just solid renewals and price adjustments. Winning large, bespoke research projects and studies is crucial. These engagements carry substantial revenue quantum and landing them consistently is key to YouGov's ability to shift into a higher growth gear. The current muted economic conditions, while perhaps not drastically impacting renewals, could potentially make securing these larger, project-based commitments more challenging. This remains a key area to watch for signs of true growth acceleration beyond the foundational subscription base. The path forward requires not just defending the core, but also successfully hunting bigger game.

Growth Acceleration: Sharpening the Tools, Revamping the Motion

While stabilization is the immediate focus, the longer-term ambition remains a return to more robust growth, targeting acceleration particularly by Fiscal Year 2026. Management isn't just waiting for the tide to turn; they've outlined a specific set of initiatives planned through the current calendar year, expressing confidence these steps can catalyze growth.

This multi-pronged approach includes tangible product enhancements like UX/UI updates and the introduction of a 'Category View' product, likely aimed at making the platform more intuitive and delivering insights more effectively within specific industry contexts. Critically, it also involves leveraging the recent Yabble acquisition to launch AI-infused products (more on this later) – a necessary move in a market increasingly focused on intelligent data analysis.

Perhaps the most strategically significant initiative, however, is the creation of a dedicated sales team specifically for Data Products. This points directly back to Shakespeare's diagnosis of strategic drift. He explicitly highlighted that the company had strayed from its original focus on a unified platform-based product and a cohesive go-to-market strategy. Establishing a specialized sales force is a concrete step to rectify this. Shakespeare sanctioning this dedicated effort signals a shift away from potentially fragmented or product-led sales efforts towards a more focused, disciplined approach targeting the core data platform.

Implementing a proper enterprise sales motion could represent a genuine unlock for YouGov. Historically, much of the growth has been product-led, which can be effective in initial market penetration but often struggles to scale revenue significantly within large enterprise accounts. A dedicated enterprise team is better equipped for navigating complex procurement processes, building C-suite relationships, and articulating a strategic value proposition that justifies larger contract values. Furthermore, management implicitly acknowledges that communicating the unique value of YouGov's Data Products against competitors has been a recent difficulty. A revamped, specialized sales effort, armed with clear messaging and potentially enhanced products (including the new AI features), is positioned as a major driver to overcome this hurdle and re-accelerate growth. This isn't just about selling harder; it's about selling smarter and more strategically into the enterprise segment.

The (Big) Yabble Bet

The centerpiece of the product roadmap appears to be the integration of AI functionality acquired through Yabble into the core Data Products suite. The strategic rationale – enhancing data analysis, automating insights, potentially creating new product tiers – has likely been articulated previously, outlining why layering AI onto YouGov's vast data asset could be highly beneficial. It promises to move beyond simple data reporting towards more predictive and prescriptive insights, a direction the entire market research industry is heading.

However, the financial structure surrounding the Yabble acquisition introduces complexity. YouGov has provisioned £3 million against the earnout for Yabble. This implies management anticipates the Yabble-derived products will generate revenues substantial enough to trigger these payments – a simple calculation based on typical earnout structures might suggest revenue expectations reaching somewhere in the vicinity of £10 million over the next three years. This signals internal confidence in the AI strategy's potential topline contribution.

Yabble contingent consideration structure

Yet, this confidence comes with a significant caveat – a double-edged sword for profitability. The earnout structure means YouGov is effectively paying out a large portion, potentially all, of the profitability generated by this new AI-driven growth in the short-to-medium term. While topline figures might improve, the quality of earnings could decline during this period as the fruits of the AI investment are shared with Yabble's former owners. This creates a lag between revenue growth from AI and its contribution to the bottom line.

Adding another layer of challenge is the competitive context. Competitors like Morning Consult reportedly launched significant AI functionality last year. This means YouGov, despite the Yabble acquisition, is essentially playing catch-up. While integrating Yabble's tech may allow them to leapfrog certain development stages, they are entering an AI race where key rivals already have established offerings in the market. Success will depend not just on the quality of the integrated technology but also on the speed of integration and the effectiveness of the go-to-market strategy for these new AI features, spearheaded by that revamped sales team. It's a high-stakes bet on both technology integration and market timing.

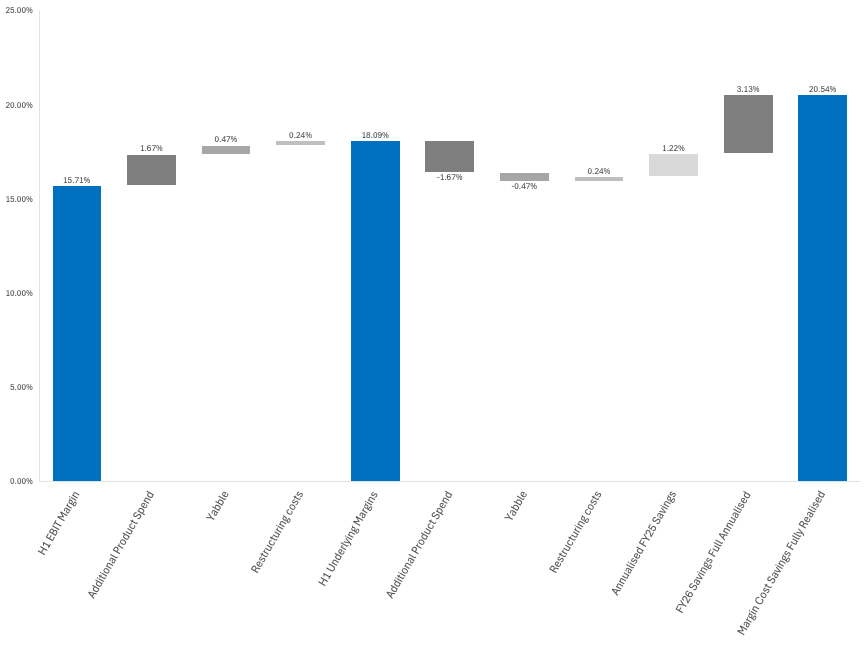

Margin Manoeuvres: Seeing Through the Noise

On the surface, margins showed only a slight optical increase, which might seem underwhelming given the focus on efficiency. However, this headline number obscures significant underlying movements and investments flowing through the P&L during the period. Several factors weighed on reported profitability: the costs associated with the redundancy program, a shift in how certain costs are capitalized, the integration of losses from the newly acquired (and not yet fully revenue-generating) Yabble, and additional investments made into the panel infrastructure.

Estimates suggest these items collectively added approximately £4.5 million in costs during the period. Stripping out these largely one-off or investment-related expenses reveals a more robust underlying margin picture, estimated closer to 18%. This adjusted figure is significantly ahead of expectations and paints a healthier picture of the core business's profitability.

YouGov Cost Saving EBIT Margin Bridge

Looking ahead, the margin trajectory appears positive. A substantial £8.3 million in cost savings from the restructuring program initiated earlier are still expected to be fully realized over the next 18 months. This provides a clear pathway for another material step-up in profitability, independent of revenue growth. Furthermore, many of the additional costs incurred in the first half (like redundancy charges and potentially initial Yabble losses) are fixed or non-repeating. This creates significant operational leverage: as YouGov potentially returns to growth, a larger portion of that incremental revenue should fall directly to the bottom line, assuming the cost base remains disciplined. This combination of banked cost savings and operating leverage is a potent recipe for significant earnings growth if the top line stabilizes and begins to recover.

However, one specific risk looms over the margin outlook: the roll-off of Transition Service Agreements (TSAs) related to the GfK CPS acquisition. While necessary for integration, the conclusion of these agreements, under which GfK currently provides certain services, is projected to create a margin headwind of approximately 4 percentage points. This needs to be factored into forward-looking margin expectations and underscores the importance of achieving the planned cost savings and leveraging growth to offset this specific pressure point.

The remaining integration of the GfK Consumer Panel Services (CPS) business represents arguably the largest operational challenge and execution risk for YouGov in the near term. While the strategic rationale for the acquisition might be sound, the practicalities of merging two complex organizations are fraught with potential pitfalls.

A key area of concern revolves around the back-office and support functions currently still being handled by GfK under the aforementioned TSAs. The critical issue here is the readiness of YouGov's own internal functions, particularly finance, to absorb these responsibilities smoothly. YouGov's finance department has undergone significant transformation over the past year, and there appears to be limited external visibility into its capacity and preparedness to take on the substantial additional load from CPS when the TSAs expire. Any disruption in these core functions could have ripple effects across the business.

The sheer size of the CPS business exacerbates this risk. Its different, often lumpier billing cycle compared to YouGov's core subscription model has already had a noticeable impact, dragging down YouGov's overall cash conversion by nearly 20% during the reporting period. This highlights the different operational cadence of CPS and the adjustments YouGov's systems and processes need to make. Integrating a business of this scale requires meticulous planning and execution. Management acknowledges the integration must be handled carefully, and it's undeniable that significant execution risk persists over the next six months as these transitions occur.

CPS: The Overlooked Engine

Despite the integration risks, the underlying performance and strategic value of the CPS business appear increasingly strong, potentially representing a significant misperception by the market. Investors have largely viewed the acquired CPS business through the lens of its legacy parent, GfK, seeing it as a low-growth, perhaps structurally challenged entity. The irony, however, is stark: CPS is currently YouGov's fastest-growing segment. CFO Alex MacIntosh summarise CPS’s performance well

“I want to make the point that overall its been a very uncertain macro environment that we are trading in. And 5% growth in mostly FMCG and retail really speaks to the strength to products and data that CPS has.”

This performance should alleviate some investor concerns about the acquisition rationale. Far from being a decaying asset, CPS appears to be a robust, highly recurring business. Its stability and scale are underscored by its contribution of approximately £28 million in EBIT annually to the combined entity. This is a significant baseline of profitability.

Regardless of one's view on the long-term growth prospects for consumer panel data, the immediate financial impact is undeniable. The substantial cash flow generated by CPS provides YouGov with significant additional resources. This enhanced free cash flow generation will eventually deleverage the balance, provide capacity for further investment, and potentially enable significant shareholder returns or further M&A down the line. The sheer financial weight CPS brings to the table should not be underestimated, even before considering future synergies.

The synergy potential between YouGov and CPS also raises the prospects of the real prize, additional growth opportunities for CPS. Management is actively exploring multiple avenues to leverage the combined entity's strengths, suggesting a future where CPS is not just integrated, but actively contributing to broader group growth.

One obvious path is geographic expansion. Leveraging YouGov's existing footprint and potentially overlapping panel assets could allow for the efficient rollout of CPS offerings into new European markets, creating a larger, more valuable European panel proposition.

YouGov/CPS Panel Overlap

A second vector is the development of a new proposition specifically for the US market. While details weren't fully announced at the results presentation, the fact that management is already actively hiring for a dedicated US team for CPS indicates this is a near-term priority. Cracking the lucrative US market more deeply with the CPS offering would be a major win.

Perhaps the most compelling synergy lies in cross-selling. CPS customers, on average, are larger organizations than YouGov's traditional client base. This presents a significant opportunity to introduce YouGov's suite of Data Products and Custom Research capabilities to these large CPS clients, potentially opening doors that were previously harder to access. This strategy appears to be gaining traction internally, evidenced by key leaders from the legacy CPS business taking on prominent roles within the wider YouGov group structure, such as the DACH CEO and the Germany Country Manager positions. Placing leaders with deep CPS client relationships into broader YouGov roles is a clear signal of intent to drive this cross-selling motion.

Considering these multiple avenues – geographic expansion, a dedicated US push, and synergistic cross-selling – the acquisition of CPS starts to look less like just bolting on earnings and more like acquiring a platform for future, potentially accelerated, growth for the entire YouGov group. There are numerous options available, painting a picture of an improved growth profile going forward, contingent on successful integration and execution of these synergy strategies.

The Investment Case: Pricing for declines, potential for growth

Putting it all together, the current market valuation of YouGov seems heavily influenced by recent challenges, it now trades on just 9x P/E, 5.6x EV/EBITDA, a ~14% FCF yield and 4% dividend yield. In essence, the market is pricing the company akin to a structurally challenged business facing irreversible decline. This perception, however, appears increasingly misaligned with the strategic direction being set by returning CEO Stephan Shakespeare.

Shakespeare has articulated a clear strategy focused on returning YouGov to growth. This isn't based on wishful thinking, but on leveraging the company's core competitive advantages – its proprietary panel data, technology platform, and brand reputation. There's a stated commitment to investing in the business, particularly in product development (AI integration) and the crucial go-to-market engine (dedicated sales force).

While acknowledging that a return to historical growth levels won't happen overnight and requires diligent execution, several factors provide a foundation for future performance and potential upside. The high renewal rates in the core Data Products business also offer stability to the estimates going forward. The significant cost restructuring program then provides a clear path to improved profitability and operational leverage in the near term.

The conviction displayed by management, coupled with a strategy that appears logical and builds on inherent strengths, stands in contrast to a market valuation that seems to be discounting virtually any prospect of future growth. While execution risks, particularly around the CPS integration, remain real, the overall trends – stabilizing sales, underlying margin improvement, unlocked cost savings, and clear growth initiatives – appear to be pointing in a more positive direction.

From this perspective, the current valuation looks compelling. The market seems focused on the rearview mirror, while management is attempting to steer the company towards a more promising horizon. If Shakespeare and his team can successfully navigate the integration complexities and execute on the outlined product and sales strategies, the disconnect between current pricing and future potential could narrow significantly. The foundation seems to be setting; the question is how quickly and effectively YouGov can build upon it. I am using this point to build upon my position, adding shares post results.