From subdued guidance to the competitive moat: Answering all the Trainline questions

Trainline's recent share price performance has, to put it mildly, underwhelmed, leaving many investors with a litany of pressing questions regarding the company's trajectory and the resilience of its business model. The narrative has been dominated by concerns over slowing growth and structural market shifts, prompting a deeper dive into the underlying health and future prospects of this digital travel aggregator. In order to re-underwrite the investment case in light of these concerns, I have attempted to answer investors' questions starting with the recent full-year results and culminating in a reassessment of Trainline’s competitive moat.

Summary

Temporary Headwinds Mask Medium-Term Strength: While FY26 revenue guidance is subdued due to specific, time-bound factors like take-rate adjustments and initial PAYG impacts, these are expected to annualize, paving the way for a potential growth re-acceleration to the 5-7% range in the medium term.

Structural Concerns Addressed, Not Insurmountable: Key investor anxieties around GBR competition and PAYG expansion have credible answers. GBR's timeline is distant, its impact on an entrenched incumbent like Trainline is debatable, and Trainline is proactively developing solutions to participate in the evolving PAYG landscape.

Aggregator Moat Underappreciated: The market seems to be underestimating the durability of Trainline's powerful aggregator moat, built on direct user relationships, comprehensive supply integration, strong network effects, and a superior user experience, which are difficult for competitors to replicate.

Valuation Disconnect Presents Opportunity: The current valuation reflects an overly pessimistic view, trading on just 7x EV/EBITDA and 15x for a business still producing LDD earnings growth via margin expansion. This mispricing offers an attractive entry point for long-term investors.

FY2025 Results

Trainline’s 2025 full year results, at first glance, paint a picture of continued progress: revenue up a respectable 11% to £452 million, UK sales up 10%, and an EBITDA of £159 million, up 30% year-over-year, even exceeding analyst expectations. EBITDA performance implies a 2.69% margin on net ticket sales, up from 2.31% the prior year, driven by better gross margins and operating leverage.

The specter haunting this otherwise solid report was guidance for FY26. Trainline’s FY26 revenue guidance is that Trainline expects net ticket sales to grow between 6% to 9% for FY2026. Revenue growth is expected to be slower than net ticket sales, in the range of 0% to 3%. Consensus expectations for revenue growth were around 3.3%. The reaction from investors was a familiar narrative; Trainline is facing structural headwinds to its growth with incredible risks for the business going forward. Given the continued weakness in the share price, I have attempted to re-examine Trainline’s growth prospects for FY26 (including the factors driving this weaker guidance), the structural questions investors hold, and ultimately Trainline’s moat itself. While there are still immediate headwinds, there are answers for the longer-term strategic questions.

Lacking near-term growth momentum (for now)

The first point I have to acknowledge is that after its guidance Trainline will show low growth momentum throughout the next fiscal year. The key question is not merely what Trainline reported, but why the outlook is tempered. There are two factors causing the revenue headwind in FY26:

A 50bps take rate reduction: In 2022, the Rail Delivery Group, as part of a review into the UK rail industry, cut the industry take rate for retailers from 5% to 4.5% (a 50bps reduction). This is being implemented alongside a reduction of 25bps in industry costs.

Pay-as-you-go (PAYG): TfL has expanded its Pay-As-You-Go system to commuter routes further outside London. Trainline has estimated that this puts £150m, or 2.5% of its net ticket sales, at risk.

Crucially, these are not indefinite drags on Trainline's UK operations but rather specific, time-bound adjustments. The take rate reduction, stemming from an industry-wide review, is positioned as a one-off event; subsequent reviews have not indicated further cuts, suggesting this particular headwind should annualize and thus conclude its impact within FY26. Similarly, while the expansion of TfL's PAYG system does introduce a direct alternative for certain commuter journeys, its current quantifiable impact is on a relatively small portion of Trainline's total net ticket sales. The future trajectory of PAYG's encroachment remains a point of observation, but it is not, as of now, an existential threat to the broader business (more discussion on the long-term threat is included later).

Trainline’s guidance does not totally remove all the risk associated with these headwinds, but I do believe that it incorporates a very conservative scenario. I estimate that the low end of Trainline's guidance is assuming an £150m headwind from Pay-As-You-Go offset by an improvement in the international segment's revenue growth to 10%. This is conservative as it assumes Trainline loses all of the at risk revenue from PAYG while the international business only sees a modest step up in growth.

Trainline’s FY26 guidance also masks the fact that passenger volumes are growing 3-4% in the UK (reaching 90% of their pre-COVID peak) and the benefit from circa 4.5% rail ticket price increases. The variability in the guidance is going to be the main driver of Trainline’s share price in the near-term. By Trainline's H1 results in September, we should have a good understanding of how Pay-As-You-Go trends are working out, if a step up in European growth has materialized, and ultimately what this implies. Should trends be worse than expected, it's evidence of a deeper issue and likely a reason to exit the name. However, should Trainline be able to deliver, it likely marks a turnaround point for growth.

Looking beyond the immediate FY26 horizon, the foundation for a more robust UK growth trajectory for Trainline appears surprisingly solid, despite the prevailing narrative of structural impediments. Once these current, identifiable headwinds annualize, the path clears considerably. The much-discussed Great British Railways (GBR) competitor, for instance, is not anticipated to launch its services before February 2027, removing it as an immediate drag on FY27 prospects. Similarly, further significant expansions of the Pay-As-You-Go system, beyond those already factored in, have not been outlined, let alone implemented. This suggests that, absent new, unforeseen pressures, the underlying positive dynamics of the UK rail market should become the primary drivers of Trainline's domestic performance. Consequently, it is plausible to envision a scenario where, within a year, UK growth expectations for Trainline could reset to a healthier 5-7% range, a stark contrast to the current 0-3% guidance. Even if one were to conservatively model another £150 million headwind from a hypothetical further PAYG expansion, the resultant revenue growth would likely still settle in the 3-5% bracket, significantly outpacing the top end of current market expectations for the upcoming year. This underscores a potential disconnect between short-term sentiment and medium-term fundamental prospects.

Structural Questions have answers

Beyond the immediate financial performance, the deeper structural questions facing Trainline preoccupy the minds of most investors. Encouragingly, Trainline's recent annual results provided a substantive degree of clarity on how management perceives and is actively addressing these dynamics. An examination of the company's commentary is therefore warranted, as it offers a valuable response to some of the more persistent investor anxieties.

The most prominent structural concern, particularly for its core UK market, is the advent of Great British Railways (GBR). GBR aims to be a new, single guiding body for railways in Great Britain, with a mandate to simplify fares and improve the passenger experience. The concern is that GBR could become a formidable, state-backed competitor, potentially marginalizing independent retailers like Trainline. The GBR's own ticketing app or website, if developed and promoted effectively, could directly challenge Trainline's market share, especially if it offers benefits that third parties cannot match (e.g., exclusive fares, integrated journey planning across all services by default).

However, the GBR situation is complex and not necessarily a purely negative development for Trainline. To begin with, GBR is not due to be set up until 2027, with work on its own ticketing solution unlikely until the end of the decade. This extended timeline provides Trainline with a significant window to further entrench its position, innovate, and demonstrate its value. Moreover, even when a GBR retailer eventually materializes, the path to dislodging an established incumbent like Trainline is far from straightforward. CEO Jody Ford, on the earnings call, highlighted the significant network effects at play in the market, which have historically made it challenging even for well-funded competitors to gain substantial traction.

“We have faced a number of different competitors over the last few years, and most recently Uber coming into the market, what, nearly three years ago now. That’s a very well-funded West Coast tech company, which got the number two travel app [in the UK] and a large user base. And after three years we see them at less than 2% in terms of market share.''

Concerns from some investors also tend to overlook Trainline's already formidable market share and the inherent stickiness that comes with being the dominant, established ticketing aggregator. Furthermore, any successful GBR offering would likely coincide with a broader industry push to transition more passengers from offline to online ticketing channels. Given that nearly half (48%) of the UK rail market still operates offline, growth for a GBR platform would not necessarily equate to a direct, one-for-one loss of share for Trainline; much of it could come from this offline segment. Ultimately, GBR would need a fundamentally differentiated approach, not just marginally better features, to overcome the inertia and accumulated advantages that Trainline, as the incumbent aggregator, currently enjoys.

A second structural concern centers on the expansion of Pay-As-You-Go (PAYG) contactless ticketing systems to more locations across the UK. A government-backed trial is already planned in areas like Manchester and the West Midlands with ambitions for further rollout. The apprehension is that as PAYG becomes more ubiquitous, it could erode Trainline's relevance, particularly for the lower-value short-distance, and commuter journeys that are most amenable to a simple tap-in, tap-out system. While it's true that PAYG directly addresses this segment of the market, it's crucial to understand its limitations and Trainline's strategic response. PAYG, by its nature, does not cater to advance ticket purchases, which constitute the majority of Trainline's revenue and often involve more complex itineraries or seat reservations that benefit from an aggregator's interface. More significantly, Trainline is not passively observing this trend; it is actively developing capabilities to integrate with and even win PAYG-related revenue through its "Trainline Solutions" segment.

Trainline Solutions offers operators the intriguing possibility of implementing GPS-based PAYG systems, thereby sidestepping the significant capital expenditure associated with physical gate installations by leveraging app-based tracking instead. This technological pivot could play directly to Trainline's strengths, as its widely adopted app can deliver substantial user demand to such a system. This proactive approach, offering its technology to enable or enhance PAYG systems, keeps Trainline relevant as a supplier no matter the ticketing landscape; it is not the existential threat that some investors perceive.

The outlook for Trainline's international business appears increasingly favorable, potentially dispelling lingering concerns about its growth prospects in these markets. Several factors contribute to this renewed optimism: the evolving landscape of AI in search is reportedly driving renewed traffic towards Trainline, offering a pathway to recover growth previously impacted by Google's page ranking adjustments. Ford commented:

“Google is having significantly more AI features, it's not just about a rail module. And that means that SEO is being pushed down the page. I think what’s pretty interesting and exciting for us is that we are indexing very well on those areas of AI…..While it’s not yet meaningful at a great scale, it's grown 3x since January, the number of clicks. So it's growing very, very fast. And I think within the next six to 12 months it will become meaningful at a kind of SEO scale that grows faster.”

Ford's commentary here is particularly noteworthy. If Trainline can indeed capture significant traffic from these AI-powered search features, it could represent a crucial counter-narrative to the headwind risk posed by Google, potentially turning a perceived threat into a new avenue for customer acquisition. This could have the potential to transform Trainline’s international growth.

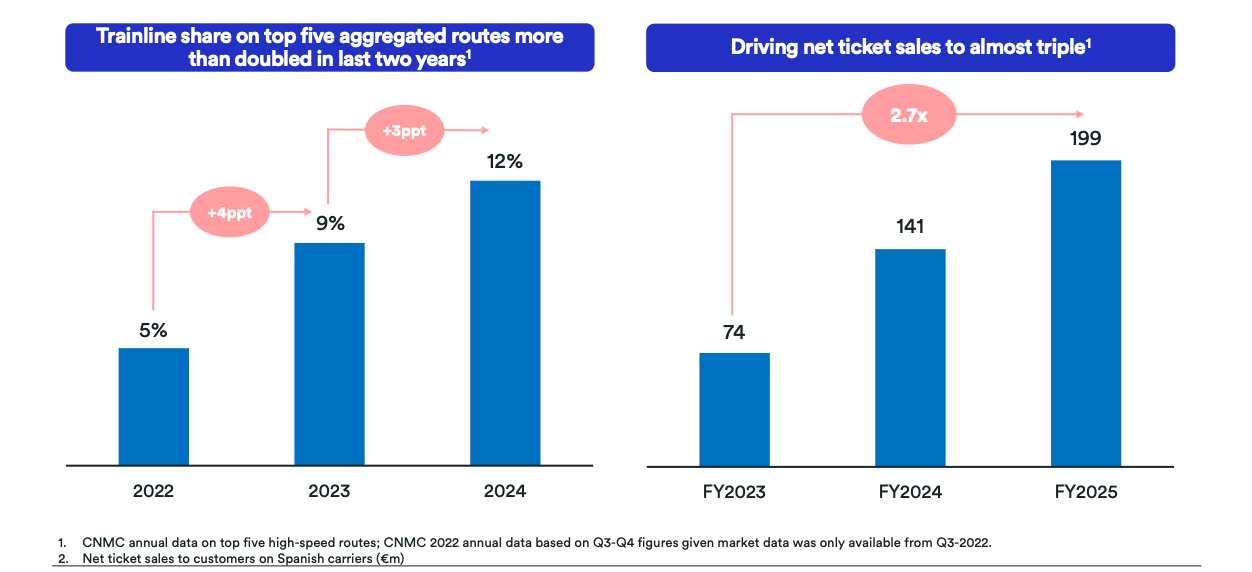

Furthermore, Trainline possesses a proven ability to capture market share in liberalizing European markets, a trend now emerging in larger European territories where its brand recognition is more established. In Spain, Europe most liberalised market, Trainline’s has seen significant market share gains and large ticket sales growth as a result of more competition between train operators.

Liberalsation is now about to intensify in France and Italy—markets that constitute 70% of Trainline's international business and where its brand recognition is considerably higher. Changes in these market is therefore poised to make European market liberalisation significantly more meaningful for the company. Ultimately France and Italy will have a larger and faster impact on Trainline’s international segment than Spain has, providing a substantial boost to overall company growth.

While the full realisation of European growth has undoubtedly been deferred in recent years, the underlying trajectory is positive and accelerating, indicating that the strategic direction is sound and that momentum should continue to build.

Does Trainline still have the power of an Aggregator? Reassessing the Moat

Given the headwinds Trainline has been facing, I believe it is prudent to re-examine Trainline’s competitive moat. Trainline substantially embodies the characteristics of an online aggregator in the rail and coach travel sector, something that confers a massive competitive advantage.

It has successfully established a direct relationship with a large user base, primarily through its dominant mobile application, and aggregates a comprehensive supply of travel options from numerous carriers. This position affords Trainline powerful network effects, a growing data moat leveraged for service personalization, and strong brand recognition. However, does the recent lackluster performance indicate these advantages are weakening? In essence, is Trainline losing the power of aggregation?

The internet, by making the distribution of digital information virtually free and abundant, has shifted the locus of power. The new scarcity is not content or service availability, but rather user attention and engagement. Platforms that effectively aggregate this attention and own the user relationship become the new gatekeepers, reversing the traditional leverage held by suppliers or distributors.

Trainline displays a number of these characteristics:

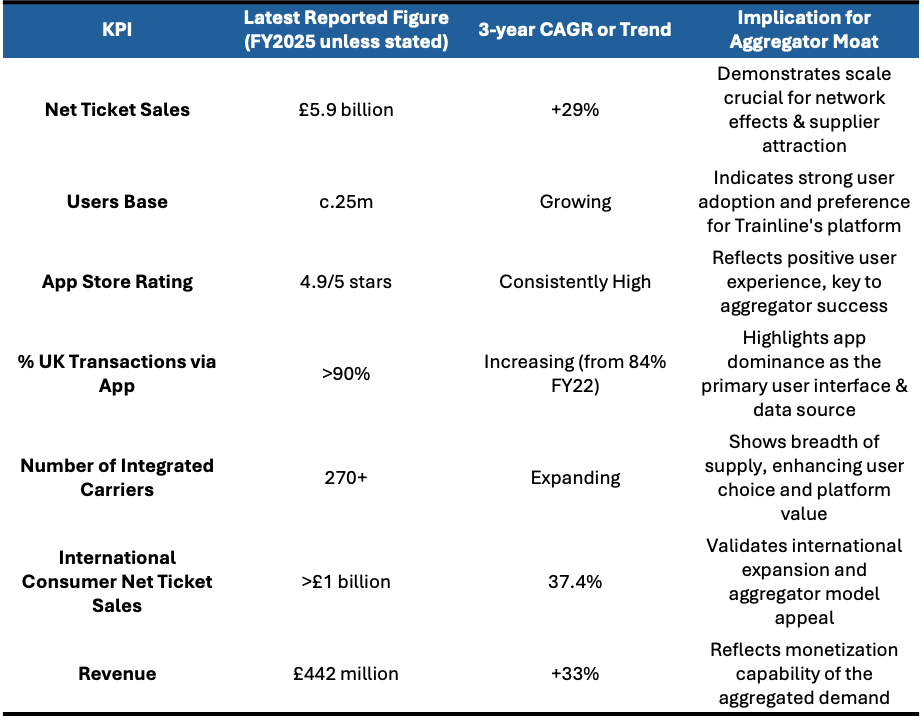

Establishing and Owning the User Relationship: Trainline has successfully cultivated a direct relationship with millions of travelers. This is most evident through its mobile app, which has over 55 million downloads. Critically, over 90% of its UK transactions are conducted via this app. This high level of engagement through a proprietary platform signifies ownership of the customer interface, a cornerstone of aggregation.

Aggregating Supply: Integrating 270+ Carriers: Trainline's comprehensive integration of 270+ rail carriers has aggregated the supply in the rail sector. Such supply provides users with a broad array of choices and the convenience of comparing them on a single platform. This breadth is fundamental to an aggregator's value proposition.

Focus on User Experience (UX): Platform features, AI, real-time info: Trainline explicitly emphasizes its commitment to delivering a superior user experience. The goal is to provide "an unrivaled set of journey options" and simplify complex travel planning; this utility provided to users retains demand, a key feature of aggregation.

An aggregator builds a strong competitive moat primarily through powerful network effects. Once an aggregator establishes a direct relationship with a critical mass of users by offering a superior experience, it becomes indispensable to suppliers who need to reach that audience. More suppliers enhance the platform's value, attracting even more users. This virtuous cycle creates a formidable barrier to entry, as competitors struggle to replicate both the user base and the breadth of supply simultaneously, leading to winner-take-all or winner-take-most dynamics.

Trainline displays most of these characteristics, which, whether rooted in its network effects, substantial data assets, or strong brand recognition, are considerable and not easily replicated. These advantages are further buttressed by structural industry trends, such as the ongoing liberalization of European rail markets, which increases the consumer need for a simplifying aggregator, and the persistent shift towards digital ticketing and mobile-first solutions. This was wonderfully articulated by CEO Jody Ford during the FY25 results call:

“I think it's always worth remembering like the unique inventory we bring in terms of cross border travel inbound is really, really special and very hard to get. And actually many of those customers that we’re bringing from the UK, from the US, increasingly from those domestic bases that we’re building up across Europe into other European countries, almost wouldn’t buy rail travel if we didn’t make it so easy.”

He also outlined the impact for both operators and Trainline’s take rate from this dynamic:

“[In the Spanish market] We have seen that effectively our take rate has continued to go up as we have understood that we actually can provide double-digit share for them [Train operators]. And as that goes forwards, actually they begin to bake that into their models and they continue to meet those customers as they go forwards into the following year.”

The structural questions examined do present challenges, but they do not undermine Trainline’s aggregator strengths for the simple reason that they do not remove the demand that Trainline already controls within the market.

The threat from GBR is a long-term consideration, but Trainline's incumbency and the historical difficulty new entrants have faced suggest its moat is not easily breached.

The rise of PAYG is a manageable challenge, with Trainline proactively adapting its technology and leveraging the demand it already controls to provide PAYG services.

The international outlook is notably positive, with emerging trends like AI in search and ongoing market liberalization acting as potential tailwinds that reinforce and expand its aggregator model.

The KPIs underlying Trainline’s performance demonstrate that for all the structural concerns, demand on the company’s platform remains healthy.

This demand sustains Trainline’s moat, as any potential competition still has to grapple with the difficulty of wrestling demand away from Trainline. In some aspects, particularly internationally, it also shows signs of strengthening. The company's management seems aware of the structural shifts and is actively taking steps to mitigate threats and capitalize on opportunities, leveraging its core aggregator advantages.

Still an Opportunity in the Mispricing?

The market's current appraisal of Trainline, as I've noted previously, appears to reflect a perception of a business in decline, a narrative that seems increasingly at odds with the underlying fundamentals and strategic positioning. I must concede that the short-term growth headwinds have proven somewhat more pronounced and opaque than perhaps I initially anticipated, making the immediate future more challenging to navigate. However, to focus solely on these transient difficulties is to overlook the enduring strengths of a business characterized by excellent economics and substantial, long-term growth opportunities, particularly as it solidifies its aggregator position in an evolving European market. Furthermore, downgrades that followed the recent full-year results have only served to widen the valuation discount when compared to its peers, despite the company demonstrating resilience in key areas.

Trainline now trades 7.1x EV/EBITDA, a 40% discount to European digital platform peers. Furthermore c14x PE is attractive on an absolute basis. For all the revenue concerns Trainline is still producing MSD EBITDA growth and LDD EPS, through expanding margins.

It is this disconnect – between the current, arguably pessimistic, market valuation and the intrinsic, long-term value proposition of a dominant platform aggregator – that informs my decision to add to my position.